Given the current situation in Iran, we wanted to send you all a quick note on the market’s reaction, any implications for our longer-term views as well as how your portfolios have been performing.

Market Reaction

Broadly the market reaction has been somewhat subdued but there has been a lot of noise. Here are a few themes we have pulled from all the noise over the past few days:

- Commodities – energy is right at the center of the volatility due to the dependency of the Middle East economies to energy exports as well as the dependencies many nations have on those inflows. Oil prices had been increasing into the strikes on the weekend, with many adding a geopolitical premium to the cost of a barrel. Oil prices have continued to increase throughout the week while natural gas prices have been more regionally dependent. Europe is reliant upon natural gas exports from Qatar and shutdowns there have caused European natural gas prices to spike 50-100%. Gold has remained volatile with the geopolitical risk premium attached to its price, moving with the headlines.

- Currencies – the largest move across the currency markets has been the move higher in the U.S. Dollar against nearly all other currencies. The move is typical in periods where markets shift to risk concerns, with investors prizing the perceived safety of U.S. Dollars. Elsewhere the difference has really been driven by the energy dependencies of countries. Those nations or regions that are net-importers of energy (South Korea, Japan, India, Europe as examples) have seen their currency weaken more rapidly.

- Equities – areas that are energy importers have seen poor performance in their stock markets. As Gavekal (our favorite macro research firm) has said, “growth is energy transformed”. Therefore, if the price of energy increases rapidly, the cost of production does too. Stock markets such as Korea, Japan, and Europe have seen the largest drops in prices. Energy exporters such as Canada and the U.S. have performed relatively well.

- Fixed income – the government bond market had been performing well to start the year with the expectation that lower inflation would drive further rate cuts. However, the moves this week have been more focused on whether energy prices will drive inflation higher and therefore rate cuts could be put on hold or pushed out.

Portfolio Performance

The good news is that we entered March with a lot of “gas in the tank” from a performance perspective. Below are some comments on our estimated year-to-date performance across our investment strategies. Please keep in mind these are all estimates and are subject to change:

- Income: our public fixed income strategy (Sagard Wealth Income Fund) is estimated to have returned close to 0% through February. Gains in emerging market bonds were offset from losses on U.S. corporate loans. Our hedge fund strategy (Sagard Wealth Absolute Return Fund) started the year well with an estimated return of over 4% through the end of February. This portfolio is built to generate slow and steady returns and tends to protect well in periods of uncertainty. It is still very early to comment on our private credit portfolio (Sagard Wealth Alternative Credit Fund), but we estimate that it performed well in January as signs of distress in credit markets increased the opportunity set for those managers focused on stressed sectors. All in all, we believe we are running in line or beyond our return targets for the income strategies.

- Growth: our active public equity strategy (Sagard Wealth Thematic Equity Fund) started the year extremely well and we estimate it is up over 11% entering March. Gains in Canadian mining stocks, Japanese equities alongside value-biased investment managers, have helped. This compares favorably with the global equity market which has returned 3.8% over the same period. It is still too early to comment on our private equity portfolio, which has quarterly valuations.

- Preservation: our real asset portfolio (Sagard Wealth Real Assets) is designed to protect our clients from heightened inflation. We are estimating that the fund has delivered +7% through the end of February, which is far beyond our return expectations of CPI + 4%. Our heavy allocations to gold and commodities have propelled the returns.

Current View and Positioning

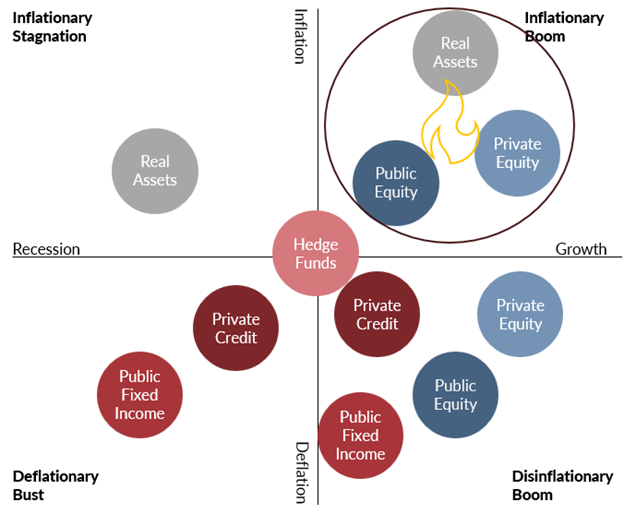

Our macro lens is driven through a relatively simple framework. Are we in a regime of stronger or weaker economic growth and are we in a period of elevated or low inflation? As we have written in the last few quarterly letters, we believe that the twin stimulating factors of corporate expenditure on AI and the related infrastructure alongside increased government spending (particularly in defence) are both pro-growth while also driving higher than normal inflation. The chart below shows this and our favoured portfolio tilts:

Has our view changed? We still see the same factors driving both corporate and government spending and therefore still support our view that we remain in an inflationary boom. There are now more elevated risks that a prolonged shift higher in energy prices does cause economic contraction, therefore shifting us to the left on the diagram into the inflationary stagnation quadrant. If this shift happens, then owning real assets is a common thread and we still think a larger allocation to that solution protects portfolios from this shift.

Otherwise, we are focused on looking for any opportunities that may arise from the volatility. As always, we are looking for the signal amongst the noise. Entering March we reduced our best performing equity theme (“Heavy Metal”) as more of a profit taking exercise. We have dry powder across most of the portfolios and are happy to wait for opportunities.

We know there will be challenges amongst the opportunities, but we remain vigilant and ready to act. Asset allocation is the most important decision when building portfolios and we believe that our conversative approach with large allocations to alternative investments allows us to navigate storms by looking at the stars for signals rather than focusing on the noise of the waves.