Stephen Harvey

Chief Investment Officer

Sagard Wealth

Wishing an early Happy Mother’s Day to all the Mums out there who will be celebrating next weekend. Maybe some of you are sitting down right now with a glass of freshly squeezed orange juice. Which, oddly enough, brings us to this week’s market topic: squeezes.

Squeezes do not just happen to citrus fruit. They happen in markets too.

One of my favourite movies of all time is Trading Places, starring Dan Aykroyd as Winthorpe and Eddie Murphy as Valentine. The big climactic scene takes place in the orange juice futures market, where Winthorpe and Valentine bet against the Duke brothers. The Dukes believe they have inside information that the orange crop will be weak, so they try to push prices higher. Winthorpe and Valentine know the real crop report will show a strong harvest, so they position for prices to fall.

It is funny, chaotic, and deeply satisfying. It also happens to be a surprisingly good lesson in market squeezes. The type of trading behaviour highlighted in the movie later helped inspire what became known as the “Eddie Murphy Rule,” designed to crack down on trading using stolen government information.

What is a Squeeze?

A market squeeze happens when too many investors are crowded on one side of a trade and then suddenly need to get out.

The most common version is a short squeeze.

That happens when investors have bet against a stock by shorting it. To close that bet, they eventually need to buy the stock back. If the stock price starts rising quickly, short sellers can panic and rush to buy it back before losses get worse. But all that buying pushes the stock even higher, which forces even more short sellers to buy.

It becomes a painful loop.

Think of it like trying to leave a crowded theatre through one small door. Once everyone realizes there is a fire drill, nobody exits gracefully.

The Hunt Brothers: the real-life Duke brothers

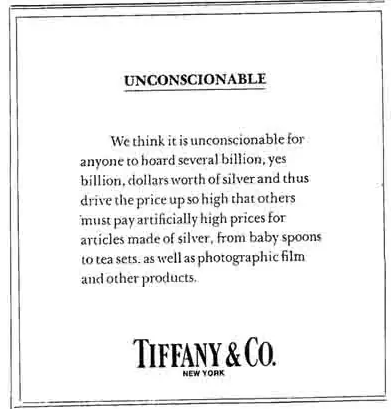

One of the great market squeeze stories involved the Hunt brothers and their attempt to corner the silver market in 1980.

The Hunts built a huge position in silver and silver futures, helping drive prices dramatically higher. Silver rose more than 400% in 1979 alone. The pressure became so intense that Tiffany & Co. even took out an advertisement in The New York Times complaining about what was happening to silver prices. When the tide finally turned, silver collapsed on what became known as “Silver Thursday.”

The story became part of Wall Street folklore, and you can see shades of the Hunt brothers in the Duke brothers from Trading Places. Same idea, different commodity. And fewer fur coats.

Volkswagen and Porsche

One of the wildest squeezes I have seen in my career was Volkswagen in 2008.

Volkswagen had two share classes: common shares and preferred shares. The preferred shares paid a higher dividend, while the common shares had voting rights. Many hedge funds looked at the gap between the two and concluded it made little sense. They bought the cheaper-looking preferred shares and shorted the more expensive common shares.

The trade looked smart on paper.

The problem was that Porsche was quietly trying to take over Volkswagen and had built exposure to a huge portion of the common shares through derivatives. Add in the stake owned by the government of Lower Saxony, and there were very few common shares left available to trade.

Suddenly, the hedge funds that were short the common shares, needed to buy them back, but there were almost no shares available. Volkswagen’s common shares exploded higher, rising roughly fivefold over just two days.

The hedge funds had focused on the dividend economics. Porsche cared about the votes. In that moment, the voting rights were not a small detail. They were the entire story.

GameStop

Then came GameStop in January 2021.

COVID had left people stuck at home, online, bored, and looking for action. There were fewer sports to bet on, more people using online trading apps, and communities like Reddit were becoming increasingly influential.

GameStop became the perfect target. It had a large, short interest, meaning many professional investors were betting against it. Retail investors piled in, often using options to increase their exposure. As the stock rose, short sellers were forced to cover, which pushed the price up even more.

The move was so dramatic that it eventually became the movie Dumb Money. GameStop rose many times over in a very short period, and several hedge funds suffered enormous losses.

It was part market event, part internet movement, and part financial food fight.

Avis: the latest squeeze

So why bring this up now?

It is not just because I watched Trading Places again last week, although that certainly helped. It is because we have just seen another squeeze, this time in Avis Budget Group.

Avis, the car rental company, saw its stock soar from mid-March into late April. The move was driven in part by the fact that two investment firms had built very large positions, leaving fewer shares freely available to trade. At the same time, many investors were betting against the stock. That combination created classic squeeze conditions: limited supply, high short interest, and suddenly everyone needing the same shares at the same time.

For a brief moment, the stock price went vertical.

But as often happens with squeezes, the elevator ride down was just as dramatic as the climb up. Avis fell sharply over two days, giving back a large portion of the gains almost as quickly as they appeared. Recent reporting described the stock as having surged more than 600% before dropping nearly 70% in a two-day selloff.

The lesson

Squeezes make for great movies, great headlines, and occasionally great cocktail-party stories. But they are dangerous places to invest.

Prices in a squeeze are often driven less by the value of the underlying business and more by positioning, leverage, forced buying, and fear. That can work beautifully for a while, but once the pressure releases, things can reverse very quickly.

The lesson from Valentine and Winthorpe is a good one: when the squeeze has done its job, take the profit, step away from the chaos, and maybe head to the beach

Preferably with a glass of orange juice.