Stephen Harvey

Chief Investment Officer

Sagard Wealth

As we are amid the Men’s 2026 FIFA World Cup, irrational exuberance could be used to define my excitement with the way both Canada and England are playing. Let’s hope that’s the final!

However, I titled this piece Irrational Exuberance as an homage to Alan Greenspan, former Chairman of the U.S. Federal Reserve, who passed away this week at the grand old age of 100. Greenspan served as the Chairman for 18 years (from August 1987 until January 2006), making him the second longest serving since inception. Greenspan famously uttered the term in 1996, as he tried to describe the performance of the U.S. Stock market

When Alan Greenspan uttered the phrase “irrational exuberance” in 1996, he managed to do what central bankers rarely achieve: move global markets with two words that sounded like they belonged in a psychology textbook and a champagne-fueled brokerage office at the same time. He was warning that investors might be bidding up stocks beyond reason, though in classic Greenspan fashion he wrapped the message in enough fog that Wall Street had to squint, panic, and then sell first. The phrase became a kind of monetary haiku for bubble behavior: everyone having a wonderful time, everyone insisting the prices made sense, and the Fed chairman standing in the corner like the sober adult at a dot-com party, gently asking whether the punch had been spiked.

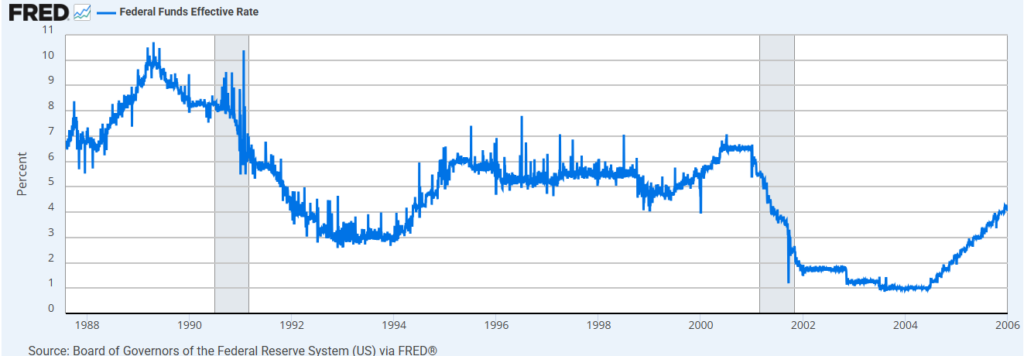

During his tenure as Chairman, the Federal Reserve was broadly on an easing cycle, with many rate cuts. The chart below shows the Federal Funds Effective Rate during his 18-year reign.

He became best known for his aggressive cutting cycle post the dot-com crash that began in 2000.

Irrational Exuberance: The Book

The term irrational exuberance became so overused from 1996, that when Robert Shiller published a book about market valuations in March 2000 (the same month the U.S. stock market peaked) it was the natural title. Robert Shiller’s “Irrational Exuberance” is essentially a polite economist walking into a roaring bull market, clearing his throat, and asking whether everyone has considered that the emperor’s new clothes may have been purchased on margin. Published just as the dot-com party was reaching its glow-stick phase, the book took Alan Greenspan’s famous phrase and built it into a full diagnosis of financial mania: investors, Shiller argued, are not always cool calculators of value but frequently excitable storytellers with brokerage accounts. Markets rise not only because earnings improve, but because narratives catch fire, neighbors get rich, journalists fan the flames, and the fear of missing out begins wearing a suit and calling itself asset allocation.

What makes the book enduring is that Shiller does not simply wag a professorial finger at foolish speculators; he shows how bubbles are social events, part spreadsheet and part group therapy session gone wrong. His great insight is that prices can become detached from fundamentals not because investors are stupid, but because humans are magnificently talented at finding reasons why this time is different, usually right before discovering that it was not. Irrational Exuberance is therefore less a scolding than a field guide to the recurring financial wildlife of capitalism: the overconfident analyst, the newly converted day trader, the permanently bullish dinner guest, and the economist quietly noting that gravity has not, in fact, been repealed.

Shiller’s Multiple

Shiller’s multiple, better known as the cyclically adjusted price-to-earnings ratio or CAPE, was created by Robert Shiller to stop investors from judging the market’s waistline after only one very flattering quarterly selfie. Instead of dividing stock prices by a single year’s earnings, it compares prices with the average of the past ten years of inflation-adjusted earnings, smoothing out recessions, booms, accounting oddities, and other market mood swings. Its interpretation is simple enough to be dangerous: when the multiple is high, investors are paying a rich price for each dollar of normalized earnings, suggesting future returns may be more modest; when it is low, the market may be offering better long-term value, or at least has stopped charging champagne prices for tap water. Like all valuation tools, CAPE is not a crystal ball as a smoke alarm: occasionally early, sometimes irritating, but worth hearing before the kitchen is fully ablaze.

So where are we today on this measure for the S&P 500 and how does that compare to 2000? The answer is, we aren’t far away from the 2000 peak. In 2000 S&P 500 peaked at a Shiller’s multiple of 44.2 in December of 1999. Today it is 41.6.

Source: multpl.com/shiller-pe

Is this time different? Can these valuations be supported by A.I driven capital expenditure?

Just like waiting to see who wins the World Cup, we will all have to wait.