Maria Isabel Vivas

Vice President, Private Equity

Sagard

Alexandre Falin

Managing Director, Private Equity

Sagard

Private equity is entering a new phase. After decades of relying on a distribution-led model in which exits funded future commitments, the asset class is now facing a structural liquidity challenge. Slower exits, longer holding periods, and a growing backlog of unrealized assets have constrained capital recycling and reshaped the fundraising environment.

In this context, the growth of secondaries, the rise of private wealth, and the adoption of open-ended semi-liquid structures (commonly referred to as evergreen structures) should be understood not as isolated trends but as interrelated responses to a reordering of the private equity ecosystem.

Open-ended private equity funds have gained strong momentum because they can offer faster deployment, vintage diversification, and a simpler way for investors, particularly in the private wealth channel, to build and maintain exposure. Yet their growth also raises important questions. Semi-liquid does not mean fully liquid, and recent redemption pressure across private market vehicles have underscored the need to look beyond headline access and redemption terms.

This paper highlights the forces driving the rise of open-ended private equity, the benefits and limitations of these structures, and the key factors investors should assess when selecting a strategy to manage private equity exposure.

01 | LIQUIDITY SHOCK IN TRADITIONAL PRIVATE EQUITY

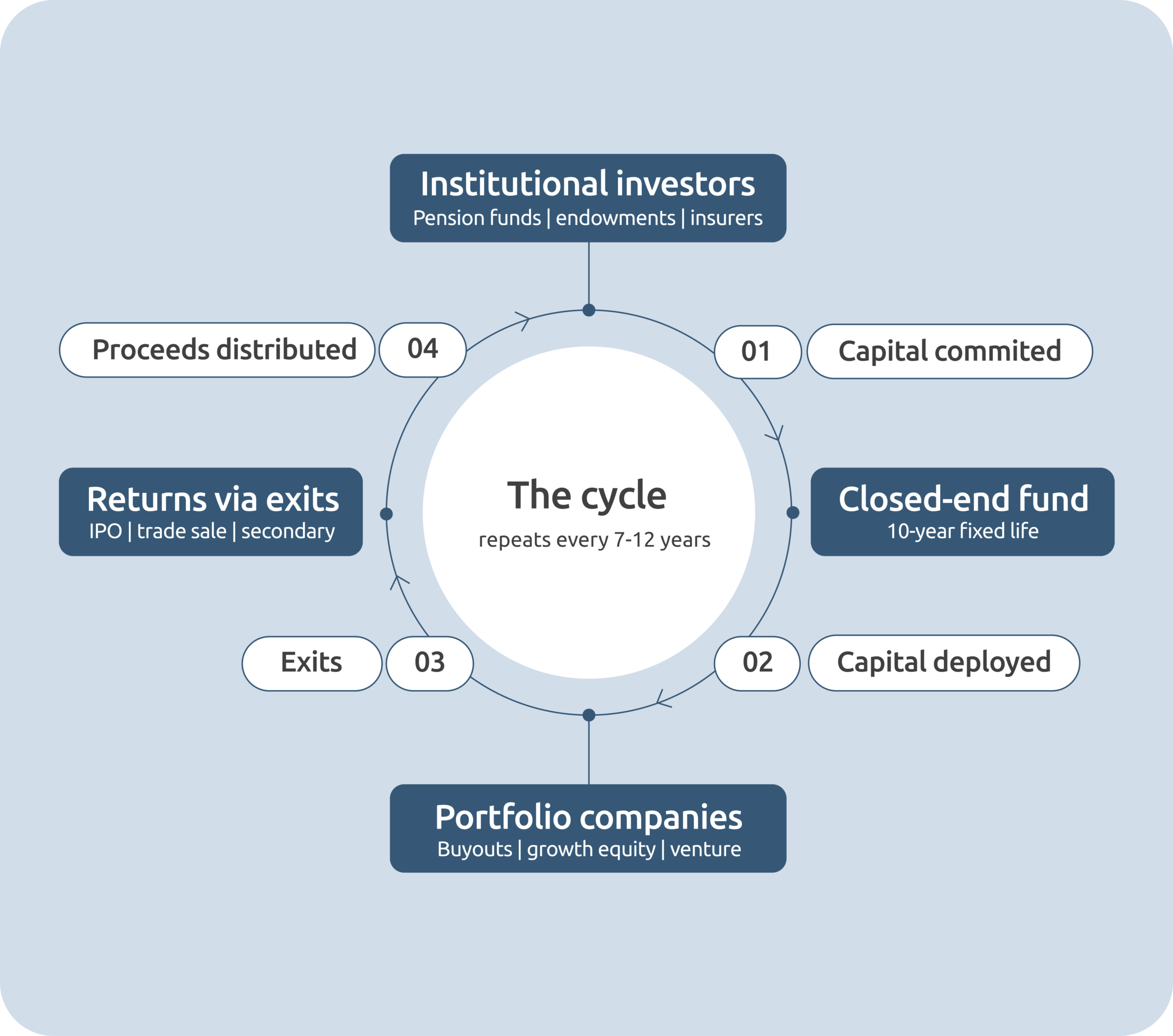

The private equity ecosystem has long depended on the cyclical flow of capital. Institutional investors commit capital to closed-end funds, which deploy it over several years, generate returns through exits, and distribute proceeds back to investors. Those distributions then help fund the next generation of commitments.

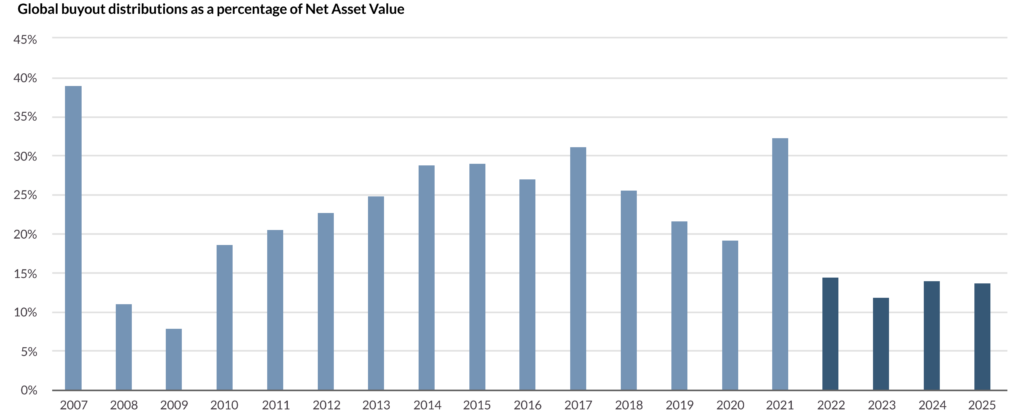

Historically, this system functioned smoothly: global buyout distributions as a percentage of Net Asset Value (NAV) typically averaged 25-35%, with peaks during strong exit environments such as 2007 and 2021.1

In recent years, however, that cycle has been disrupted. Since 2022, global buyout distributions as a percentage of NAV have fallen well below historical norms, hovering at less than 15%, reflecting a sharp slowdown in exits and a significant decline in capital returned to investors. This prolonged weakness has led to a growing backlog of unrealized assets, meaning companies that private equity funds still own and have not yet sold, so their value remains an estimate on paper rather than cash returned to investors. By 2025, there were approximately 32,000 active buyout-backed companies globally, representing an estimated $3.8 trillion in unrealized value.2 In effect, a large pool of private equity capital remains locked within portfolio companies rather than being recycled back to investors.

Source: Sagard

Source: MacArthur, Hugh. Inside Bain’s 2026 Private Equity Report. Mar. 2026

Several factors are driving this distribution slowdown. Valuation expectations remain elevated, and the gap between what sellers are willing to accept and what buyers are willing to pay continues to suppress transaction volume. Exit activity in terms of volume has weakened, with a sharp decline in IPOs since 2021. Consequently, extended holding periods have become more common: the average time to exit has risen to roughly seven years, with about 40% of portfolio companies now held for more than five years.3

The result is a liquidity bottleneck within private equity. Capital remains tied up in existing investments rather than being returned through exits, constraining investor allocations, pressuring fundraising, and increasing the need for alternative liquidity solutions and new sources of capital.

02 | NEW LIQUIDITY CHANNELS: SECONDARIES AND PRIVATE WEALTH

Two mechanisms have emerged rapidly in response.

The Secondary Market

The first is the secondary market, which has expanded rapidly, providing both General Partners (GPs) and Limited Partners (LPs) with an increasingly important liquidity valve for private equity holdings. LP-led transactions allow investors to sell fund stakes to secondary buyers, generating liquidity, managing exposures, and redeploying capital before underlying assets are realized. Meanwhile, GP-led transactions, particularly continuation vehicles, have become a major innovation by allowing managers to hold high-quality assets for longer while giving existing LPs the choice to cash out or roll into a new vehicle.4 Reflecting these dynamics, secondary transaction volume across both LP-led and GP-led deals has grown materially over time and accelerated sharply since 2022, with market volume increasing at an approximate CAGR of 30% between 2022 and 2025.5

Private Wealth

Historically, private equity has been dominated by institutional investors such as pension funds, sovereign wealth funds, insurance companies and endowments. Yet the global private wealth market is vastly larger than the institutional investor base, representing over $200 trillion in total assets held by high-net worth and mass affluent investors alone. High-net worth individuals controlled approximately $127 trillion in total assets in 2024, while mass affluent investors held an additional $100 trillion, together far exceeding the total potential financial assets of traditional institutional investors ($117.4 trillion).6

Despite this scale and projected growth in total assets of high net worth and mass affluent investors expected to reach more than $326 trillion by 2030, private wealth remains relatively under-allocated to private markets.7 While institutions allocate 25% to alternatives on average, financial advisors allocate only 5% on average to alternatives on behalf of their clients.8

At the same time, adoption of illiquid private market strategies within the wealth channel remains limited. Surveys indicate that only 31% of financial advisors currently invest in illiquid alternatives for their clients, meaning that approximately69% allocate nothing at all to these strategies.9 Despite its scale, private wealth remains under-allocated to private markets. Advisors cite five main barriers to allocating capital to private markets10:

- Illiquidity

- Fees

- Access constraints

- High minimum investment requirements

- Complexity of maintaining private equity exposure over time11

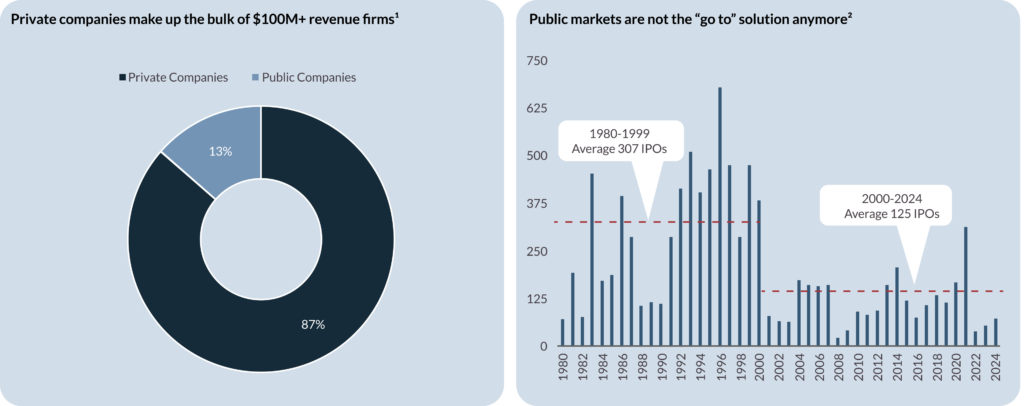

Private equity has become increasingly relevant for private wealth investors because it offers access to a broader and more differentiated opportunity. A growing share of economic activity sits outside public markets, and the number of listed companies continues to decline: most companies generating more than $100 million in revenue are private12, and the number of listed companies and IPO activity has declined significantly.13As a result, investors seeking access to the real economy are increasingly required to look beyond public equities.

Source: 1) iCapital, S6P Capital IQ, iCapital Alternatives Decoded, with data based on availability as of February 2023; 2) Jay R. Ritter Cordell Eminent Scholar, Eugene F. Brigham Department of Finance, Insurance, and Real Estate Warrington College of Business, University of Florida, iCapital Alternatives Decoded, with data based on availability as of Jul. 31, 2025. Note: Data as of Jul. 2, 2025, and is through year-end 2024. Analysis looks at all IPOs and excludes those with an offer price below $5.00 per share (penny stocks), unit offers, ADRs, closed-end funds, oil & gas limited partnerships, SPACs, REITs, bank and S&L IPOs, and stocks not listed on Nasdaq or the NYSE (including NYSE MKT LLC, the former American Stock Exchange). Given that certain stocks and companies have been excluded, IPO figures may be smaller than what is reported by other sources. Data is subject to change based on potential updates to source(s) database. For more information, please refer to the Index Definitions, Attributions, and Important Information sections at the end of this deck. For illustrative purposes only. Past performance is not indicative of future results. Future results.

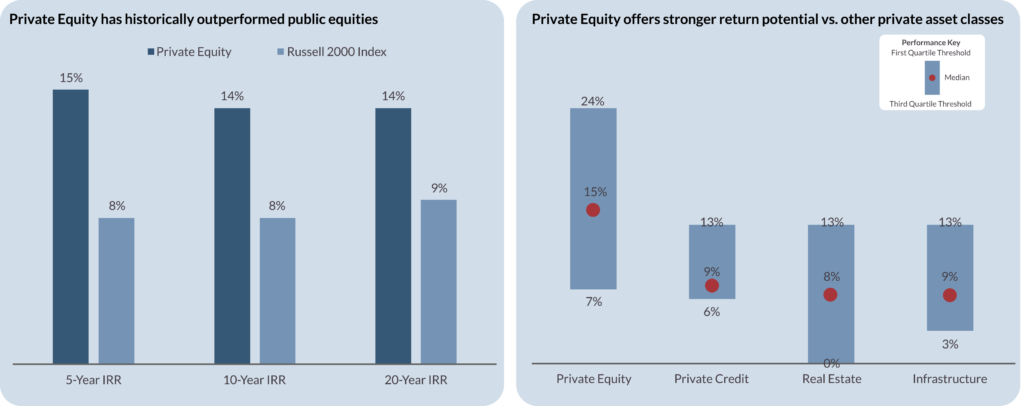

Historically, private equity has also provided a strong historical return profile relative to public equities and many other alternative asset classes, while offering a potential source of portfolio performance that is less correlated with public markets.14 This has become more relevant as investors reassess the role of traditional active listed equity strategies, many of which have struggled to outperform low-cost passive alternatives after fees. For private wealth investors, private equity can therefore offer both differentiated access to companies outside public markets and a potential complement to listed equity exposure.

Source: Data as of 31 March 2024. Benchmark is Cambridge Associates (C|A) data using Global Buyout, Growth Equity, Secondary, Funds, and Venture Capital only on Pooled Return IRR from 30 June 2004 to 31 March 2024. Russell 2000 Index IRRs are the Cambridge PME (mPME) IRR calculations of the Global Buyout, Growth Equity, Secondary Funds, and Venture Capital cash flows. ** Data as of 31 March 2024. Benchmark is Cambridge Associates data using US Buyout, US Growth Equity, Credit Opportunities, Senior Debt, Real Estate, and Infrastructure. Data shown is for the last 15 years from 30 June 2009 to 31 March 2024. Performance is shown net to investor in USD.

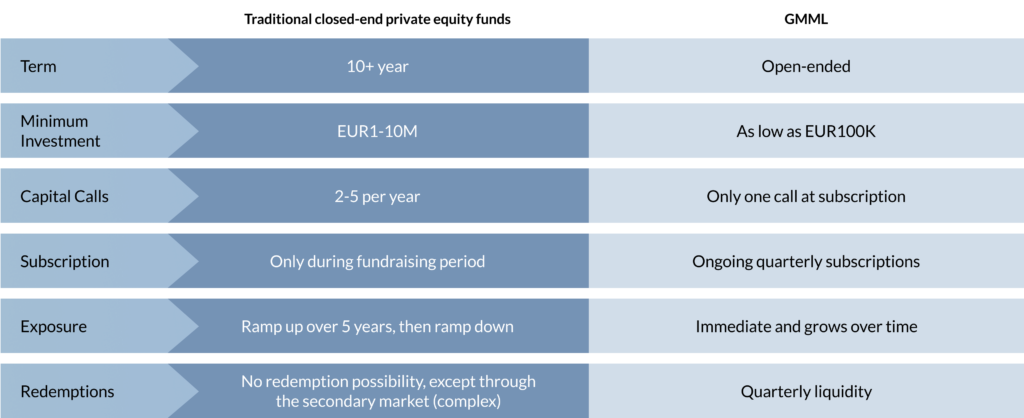

03 | THE RISE OF OPEN-ENDED SEMI-LIQUID FUNDS

A new structure has gained significant traction: open-ended semi-liquid private equity funds.15 As traditional fundraising cycles become more challenging and private wealth emerges as a key source of capital, asset managers are increasingly adopting fund structures designed to better align with the needs of wealth investors.

The potential benefits may include faster deployment, built-in diversification across vintages, and reinvestment of proceeds that could support long-term compounding.

Source: Sagard. GMML stands for Sagard Global Mid-Market Leaders, our open-ended semi-liquid fund targeting European investors.

These vehicles are well suited to the private wealth channel.

- By allowing investors to subscribe and redeem capital periodically, evergreen funds offer greater flexibility than traditional private equity structures for investors to increase and decrease their allocation.

- Moreover, they reduce the complexity and resource burden of managing a private equity portfolio, which many private investors may not have the time, scale or infrastructure to do effectively. Open-end semi-liquid funds, by contrast, are generally fully funded upfront, meaning that investors can achieve more immediate exposure, and maintain it more consistently over time given active management by the fund manager, without the need to continuously monitor distributions and recycle capital into new closed-end funds.

Despite their advantages, the term “semi-liquid” should be understood carefully: these vehicles may offer periodic redemption windows, but they do not transform private equity into a liquid asset class. Redemptions are typically subject to gates, notice periods, available cash, and the manager’s ability to protect the long-term interests of remaining investors.

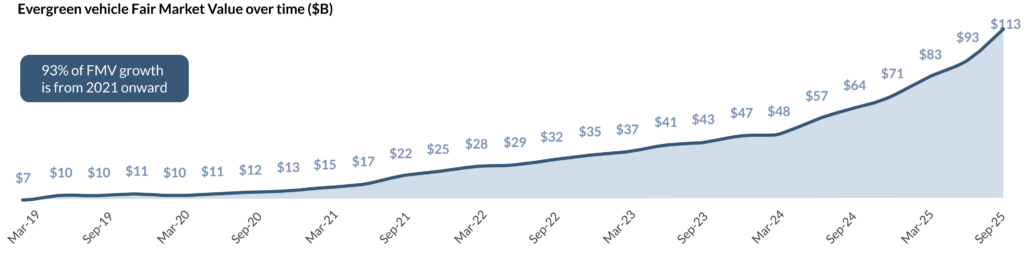

The adoption of open-ended structures has been rapid. Evergreen vehicle Fair Market Value (“FMV”) reached $113 billion as of September 2025, with 93% of that growth occurring since 2021.16

Source: Jefferies Private Capital Advisory: Semi-Liquid Investor Coverage. Mar. 2026. Fair Market Value measures the current value of assets held in evergreen structures.

This rapid growth makes fund structures more important, not less. Recent redemption pressure across semi-liquid private market vehicles has reinforced a simple point: these funds can broaden access to private equity, but they cannot eliminate the underlying illiquidity of the asset class. Their durability depends on whether growth is matched by investment quality, prudent pacing, and a liquidity framework capable of protecting investors across market cycles.

04 | SELECTING THE BEST SEMI-LIQUID FUND

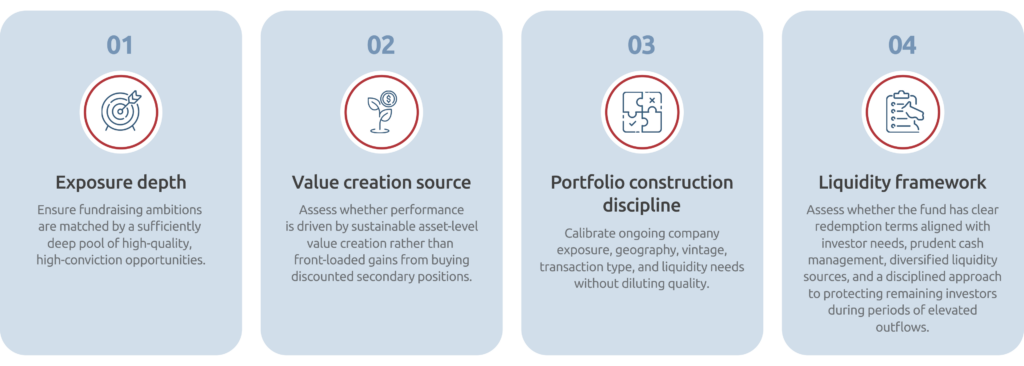

Many private equity players have launched semi-liquid structures in recent years, giving investors a wider range of options but also making fund selection more demanding. Investors should move beyond the appeal of periodic liquidity and assess how each strategy is built, managed, and stress-tested. Four areas are particularly important: the quality and depth of the underlying exposure, the source of value creation, portfolio construction discipline, and liquidity management.

Firstly, investors should assess the underlying exposure – i.e. whether the manager’s fundraising ambitions are matched by a sufficiently deep pool of high-quality, high-conviction opportunities. Growth is not automatically positive in private markets. If an evergreen fund raises capital faster than its best deal flow can absorb, the manager may face pressure to compromise on selectivity, accept lower-quality opportunities, over-diversify, or shift into adjacent strategies simply to deploy capital and avoid cash drag. The strongest funds should be able to demonstrate that their capital needs are supported by proven, repeatable, and sufficiently abundant deal flow. This is where access to excess flagship deal flow matters; it suggests that evergreen vehicles can be fed by opportunities already sourced and underwritten through the manager’s core platform, without forcing the manager to move down the quality spectrum to keep pace with inflows.

Secondly, investors should assess the fund’s value creation model. Semi-Liquid funds can generate attractive early performance when they acquire diversified secondary positions at discounts to NAV, as part of the uplift may be recognized shortly after acquisition. However, this form of value creation can be front-loaded. Once the initial discount has been captured, subsequent performance depends increasingly on the underlying asset growth rather than on the entry discount itself. As evergreen funds scale, maintaining the same return profile through discounted transactions requires an increasingly large and continuous flow of attractive secondary opportunities, supported by ongoing investor subscriptions. If inflows slow or discounted opportunities become less available, performance may moderate, potentially contributing to redemption pressure.

Investors should therefore distinguish between strategies that rely primarily on repeated discount capture and those that create value more linearly from acquisition to exit. Direct investments, co-investments and single-asset GP led transactions acquired at or around fair value can offer a different return profile, where value creation is driven by company growth, operational improvement, and eventual exit upside rather than immediate NAV uplift. Managers able to combine selective secondaries with high-conviction asset-level investments may be better positioned to deliver more durable annual gains and reduce performance volatility across market cycles.

Thirdly, investors should examine the manager’s portfolio construction discipline. Evergreen vehicles require ongoing calibration across company exposure, geography, vintage, transaction type, maturity profile, and liquidity needs. This requires the ability to combine direct investments, secondaries, and cash management in a coherent way. Direct investments can provide high-conviction exposure to attractive companies, while secondaries can support faster deployment, broader vintage diversification, and earlier visibility on value creation and exit potential. The strongest managers are those that can use these tools deliberately, rather than relying on whatever assets are available to absorb inflows. A measured growth approach, supported by a clear investment framework and proven capabilities across both direct investments and secondaries, is therefore usually more attractive than rapid scaling that risks diluting portfolio quality or weakening liquidity discipline.

Finally, investors should assess liquidity framework. In semi-liquid private markets, redemption mechanisms are designed to provide periodic liquidity, not to transform illiquid assets into liquid ones. Managers therefore need credible tools to manage outflows, including cash buffers, secondary market access, pacing discipline, and transparent redemption policies. Investors should also assess whether redemption terms are appropriately matched to the liquidity profile of the underlying portfolio. More frequent liquidity windows may appear more investor-friendly, but they can increase pressure on cash management and portfolio construction when redemption requests rise, particularly where the underlying assets are inherently illiquid. Quarterly redemption windows may therefore provide a more balanced framework, giving managers greater flexibility to manage outflows without compromising investment discipline or disadvantaging remaining investors. Investor base composition also matters: funds supported by a diversified and stable mix of investors may be better positioned to manage redemption pressure than vehicles overly reliant on a single channel or investor segment.

In that sense, the current redemption debate does not undermine the case for open-ended private equity; it reinforces the importance of careful fund selection. In recent weeks, several semi-liquid funds have announced redemption restrictions or gates, which has attracted attention. However, gates should not automatically be interpreted as a flaw. They are a structural feature designed to protect remaining investors and prevent forced selling of illiquid assets at unattractive prices. Some investors tend to overlook the “semi” in semi-liquid: these vehicles provide periodic liquidity subject to portfolio constraints, not daily liquidity on demand.

The more relevant question is why redemption pressure emerges and whether the manager has built the fund to withstand it. Rapid asset growth can become a weakness if subscriptions outpace the manager’s ability to originate high-quality investments. By contrast, disciplined growth can improve selectivity, preserve investment quality and support better long-term outcomes. This makes manager selection at least as important in open-ended private equity as it is in closed-end funds. Investors should focus not only on redemption terms, but also on the durability of the value creation model, the depth of deal flow, the discipline of portfolio construction, and the credibility of the liquidity framework.

NOTES

| 1MacArthur, Hugh. Inside Bain’s 2026 Private Equity Report. Mar. 2026. 2MacArthur, Hugh. Inside Bain’s 2026 Private Equity Report. Mar. 2026. 3MacArthur, Hugh. Inside Bain’s 2026 Private Equity Report. Mar. 2026. 4 Definitions for GP-led transactions and LP-led transactions can be found in the appendix. 5Evercore Secondary Report 2025 6PwC. “Asset and Wealth Management Revolution 2024 | PwC Global.” PwC, 2024, www.pwc.com/gx/en/issues/transformation/asset-and-wealth-management-revolution.html. Total assets represents the overall pool of potential financial assets. 7PwC. “Asset and Wealth Management Revolution 2024 | PwC Global.” PwC, 2024, www.pwc.com/gx/en/issues/transformation/asset-and-wealth-management-revolution.html. Total assets represent the overall pool of potential financial assets. 8Nielson, Darby, et al. Product Strategy Chief Investment Officer Hongshu Chen, CFA Quantitative Analyst a Study of Allocations to Alternative Investments by Institutions and Financial Advisors a Study of Allocations to Alternative Investments by Institutions and Financial Advisors | 2. 2025. | 9Nielson, Darby, et al. Product Strategy Chief Investment Officer Hongshu Chen, CFA Quantitative Analyst a Study of Allocations to Alternative Investments by Institutions and Financial Advisors a Study of Allocations to Alternative Investments by Institutions and Financial Advisors | 2. 2025. 10Nielson, Darby, et al. Product Strategy Chief Investment Officer Hongshu Chen, CFA Quantitative Analyst a Study of Allocations to Alternative Investments by Institutions and Financial Advisors a Study of Allocations to Alternative Investments by Institutions and Financial Advisors | 2. 2025. 11In practice, building and maintaining a target private equity allocation requires a complex combination of closed-end funds, which can take years during the ramp-up phase and become difficult to maintain as distributions reduce exposure. 12iCapital, S6P Capital IQ, iCapital Alternatives Decoded, with data based on availability as of February 2023; | 13Jay R. Ritter Cordell Eminent Scholar, Eugene F. Brigham Department of Finance, Insurance, and Real Estate Warrington College of Business, University of Florida, iCapital Alternatives Decoded, with data based on availability as of Jul. 31, 2025. Note: Data as of Jul. 2, 2025, and is through year-end 2024. Analysis looks at all IPOs and excludes those with an offer price below $5.00 per share (penny stocks), unit offers, ADRs, closed-end funds, oil & gas limited partnerships, SPACs, REITs, bank and S&L IPOs, and stocks not listed on Nasdaq or the NYSE (including NYSE MKT LLC, the former American Stock Exchange). Given that certain stocks and companies have been excluded, IPO figures may be smaller than what is reported by other sources. Data is subject to change based on potential updates to source(s) database. For more information, please refer to the Index Definitions, Attributions, and Important Information sections at the end of this deck. For illustrative purposes only. Past performance is not indicative of future results. Future results are not guaranteed. | 14Data as of 31 March 2024. Benchmark is Cambridge Associates (C|A) data using Global Buyout, Growth Equity, Secondary, Funds, and Venture Capital only on Pooled Return IRR from 30 June 2004 to 31 March 2024. Russell 2000 Index IRRs are the Cambridge PME (mPME) IRR calculations of the Global Buyout, Growth Equity, Secondary Funds, and Venture Capital cash flows. ** Data as of 31 March 2024. Benchmark is Cambridge Associates data using US Buyout, US Growth Equity, Credit Opportunities, Senior Debt, Real Estate, and Infrastructure. Data shown is for the last 15 years from 30 June 2009 to 31 March 2024. 15Definition of closed-end and open-ended structures and a definition of each is included in the appendix. 16Jefferies Private Capital Advisory: Semi-Liquid Investor Coverage. Mar. 2026. Fair Market Value measures the current value of assets held in evergreen structures. |

APPENDIX

LP-led secondary transactions

LP-led secondary transactions enable investors to sell their stakes in private equity funds to specialized secondary buyers, often at negotiated discounts or premiums to net asset value. In doing so, LPs can generate liquidity, actively manage portfolio exposures, and redeploy capital without having to wait for the underlying assets to be realized.

GP-led secondary transactions

At the same time, GP-led secondary transactionshave emerged as a major innovation within the market. Rather than pursuing traditional exit routes such as IPOs, strategic sales, or secondary buyouts, GPs can transfer portfolio companies into continuation vehicles backed by secondary investors. These structures allow existing LPs the option to either cash out their positions or roll their investments into a new vehicle that continues to hold the assets.

Closed-end private equity funds

Closed-end private equity funds operate under a clearly defined lifecycle. Investors commit capital upfront, which the manager draws down over several years during the investment period. Deployment of a PE portfolio takes on average ~3-5 years. Portfolio companies are typically held for several years (~5-7 years) before being exited through IPOs, strategic sales or secondary buyouts. The fund then distributes proceeds back to investors and ultimately winds down after roughly ten to twelve years. Exposure is therefore built gradually, tied to a specific vintage, and naturally declines as assets are realized and capital is returned.

Open-ended private equity funds

Open-end private equity fundsoperate differently. Rather than having a fixed fundraising period and finite lifespan, they remain open to new subscriptions over time. Capital is generally fully funded upfront at subscription and invested on a continuous basis. Instead of winding down after a predetermined term, the fund remains ongoing, and investors typically remain invested until they elect to redeem, subject to the fund’s redemption terms and liquidity provisions. As a result, investors gain exposure to a portfolio spanning multiple vintages and market cycles within a single structure.

By accepting receipt of this document and reviewing the content set forth herein, you acknowledge having read and agreeing with the following terms. The information contained herein is in summary form for convenience of presentation. It is not complete, and it should not be relied upon as such. The information set forth herein was gathered from various sources which Sagard Holdings Manager LP (“Sagard”), the investment manager of Portage Ventures, believes, but has not been able to independently verify and does not guarantee, to be accurate. Sagard makes no representation or warranty, express or implied, as to the accuracy or completeness of the information contained herein. Certain information contained herein has been obtained from published sources and/or prepared by third parties, including but not limited to companies in which Sagard clients have invested, and Sagard has not independently verified such information. In certain cases, such information has not been updated through the date hereof. All information contained herein is subject to revision and the information set forth herein does not purport to be complete. The attached material is provided to you on the understanding that you will understand and accept its inherent limitations, you will not rely on it in making or recommending any investment decision with respect to any securities that may be issued, and you will use it only for information purposes. Any investment in private markets is subject to various risks; such risks should be carefully considered by prospective investors before they make any investment decision. Each investor should consult its own professional advisors as to legal, tax, accounting, regulatory and related matters before making an investment decision. Investments in any fund sponsored by Sagard have not and will not be recommended or approved by any federal, provincial or state securities commission or regulatory authority. The foregoing authorities have not passed upon the accuracy or determined the adequacy of this summary. Like all investments, an investment in the Fund involves the risk of loss. Investment products such as the Fund are designed only for sophisticated investors who can sustain the loss of their investment. Accordingly, such investment products are not suitable for all investors. The Fund is not subject to the same or similar regulatory requirements as mutual funds or other more regulated collective investment vehicles. Sagard is registered as an investment adviser under the U.S. Investment Advisers Act, 1940, as amended. Sagard Holdings Manager (Canada) Inc. is registered as an exempt market dealer in the provinces of British Columbia, Alberta, Manitoba, Ontario, Quebec, and Nova Scotia and will act as the dealer in respect of purchases of interests in funds advised by Sagard Holdings Manager LP in the Canadian provinces in which it is registered. Certain statements and certain of the information contained in these materials represents or is based upon “forward-looking” statements or information based on experience and expectations about these types of investments. The forward-looking statements in these materials include statements with respect to, among other things, projections, forecasts or estimates of cash flows, yields or returns, scenario analyses or proposed or expected portfolio composition and anticipated future events, performance or expectations. For example, such statements are sometimes indicated by words such as “expects”, “estimates”, “believes”, “forecasts”, “seeks”, “may”, “intends”, “attempts”, “will”, “likely”, “should” or negatives thereof and similar expressions. Forward-looking statements are inherently uncertain and are not guarantees of future performance and are subject to many risks, uncertainties and assumptions that are difficult to predict. Therefore, actual events or results or the actual performance of Portage Ventures may differ materially from those reflected or contemplated in such forward-looking statements as a result of various factors. No representation or warranty, express or implied, is made as to any forward-looking statements and information and no undue reliance should be placed on such forward-looking statements and information. Sagard has no obligation and does not undertake to revise or update these materials or any forward-looking statements set forth herein, except as required by law. In addition, unless the context otherwise requires, the words “include”, “includes”, “including” and other words of similar import are meant to be illustrative rather than restrictive. The information in the attached materials reflects the general intentions of Sagard. There can be no assurance that these intentions will not change or be adjusted to reflect the environment in which Sagard will operate. Certain statements in these materials contain prior performance indication. Past performance and historic information is not necessarily indicative of future activities or returns, and there can be no assurance that Sagard will achieve comparable results. Conclusions and opinions do not guarantee any future event or performance. Neither Sagard nor any of its subsidiaries or affiliates are liable for any errors or omissions in the information or for any loss or damage suffered. No securities commission or regulatory authority in the United States or in any other country has in any way passed upon the merits of an investment in the Fund or the accuracy or adequacy of the information or material contained herein or otherwise. This information is not, and under no circumstances is to be construed as, a prospectus, a public offering, or an offering memorandum as defined under applicable securities legislation. The materials contained herein are for information purposes only and do not constitute an offer to sell or a solicitation of an offer to purchase any interest in any investment vehicles managed by Sagard. This document, which has been prepared solely for information purposes by Sagard, is confidential and is being provided to you on the express understanding that it will not be reproduced or transmitted by you to third parties without Sagard’s prior written consent. Without limiting the foregoing, you (and your employees and agents) agree that you will keep the information contained herein as provided herewith confidential and agree that you will, and you will cause your directors, partners, officers, employees, professional advisors and representatives, to use such information only for information purposes and for no other purpose and will not divulge any such information to any other party. If you are not the intended recipient of this document, you are hereby notified that the use, circulation, quoting or reproducing of this document is strictly prohibited and may be unlawful. Additional information is available upon request. All references to “dollars” or “$” are to [U.S.] dollars unless otherwise stated. All information is presented as June, 2026 unless otherwise stated. Portage Ventures® is a trademark of Sagard. All rights reserved.