Overview

After an unexciting start to the year, financial markets reacted in a decisively risk-off fashion as tensions in the Middle East escalated to direct military action and the effective closure of the Strait of Hormuz.

Prior to the military escalation in late February, financial markets were already showing signs of softening, with equities drifting lower, bond yields edging higher and oil prices gradually rising, reflecting a more cautious macroeconomic and geopolitical backdrop. Immediately following the attacks on Iran by the US and Israel, oil prices jumped swiftly and equities sold off, particularly in Europe and the US, while gold rose and the US dollar strengthened as investors shifted expectations for inflation and interest rate policy.

Private markets have remained reasonably resilient to the volatility – so far. Data shows that deal activity and exits have continued, albeit at a relatively softer pace than previously – and with a continued focus on selectivity and disciplined deployment. Early signs are that fundraising is proving more challenging so far this year, although on a more positive note, funds that have been successful at raising capital are taking slightly less time to reach a final close – 14 months in Q1 compared with 19 months in 2025, with over 80% of funds that have closed either meeting or surpassing their targets1.

As regular readers would expect, we have maintained our rigorous approach to investment and exits. We are cautious investors by nature but are encouraged both by industry reports that highlight small- and mid-market buyouts as a key focus for private equity investors in 20262, and our own experiences and conversations. We have found demand for our strategies in the market has remained strong, such as for our Emerging Managers strategy, while our investment teams continue to find both attractive investments and exit opportunities. Our Directs team is, for example, finding increasingly interesting opportunities in the growing market for mid-life transactions, which is discussed later in this letter.

Deals and exits

Global deal activity fell during Q1 2026, with 1,998 deals globally over the period compared to 2,140 deals recorded in Q1 20253. Alongside the decline in the number of deals, deal value also fell – with USD 191.0B in Q1 2026, some 20% lower than the USD 239.1B achieved in Q1 2025. North America experienced a rise in the number of deals but a drop in the value during the period. Some 1,155 deals were recorded in Q1 2026, with the aggregate deal value totalling USD 99.3B, compared with 1,346 deals in Q1 2025.

In Europe, the number of deals dropped from 785 in Q1 2025 to 523 in Q1 2026. However, aggregate deal value rose from USD 44.5B to USD 70.8B.

In Asia Pacific the aggregate number of deals dropped slightly from 365 to 324 between Q1 2025 and Q1 2026. The aggregate deal value also fell – down from USD 53.0B to USD 34.0B – a 36% decrease.

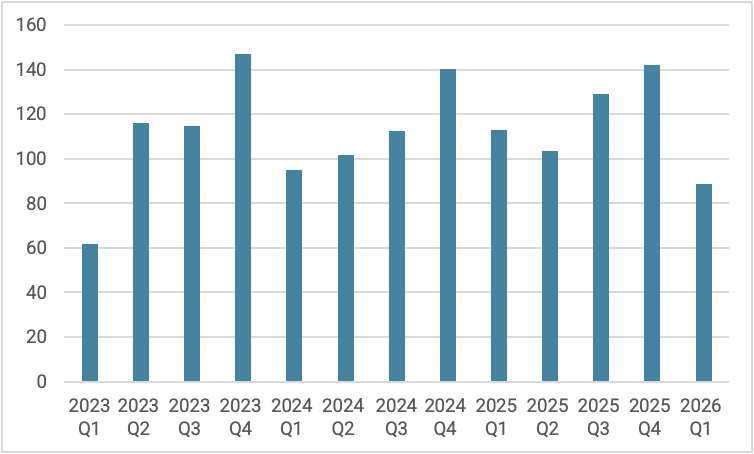

Exit activity remained subdued globally during the period with 457 deals undertaken in aggregate, down from 559 in Q1 2025. Aggregate deal value also declined from USD 112.7B to USD 88.7B over the period – a 21% decrease. Trade sales continue to be the more favourable exit route during the quarter, followed by secondary buyouts. Nine IPOs were undertaken during this period.

Figure 1: Global Exits Aggregate Deal Value (USD bn)

Source: Preqin

The number of exits in North America fell from 257 in Q1 2025 to 243 in Q1 2026, while aggregated deal value declined from USD 60.0B to USD 51.1B. In Europe, 137 exits took place during Q1 2026, down from 206 in Q1 2025. Aggregate deal value also decreased slightly from USD 35.8B to USD 25.9B. Over the same period, Asia Pacific saw exits increase, with 77 exits taking place in Q1 2026 compared with 96 in Q1 2025. Aggregate deal value dropped from USD 16.9B in Q1 2025 to USD 11.6B in Q1 2026.

1PEI Fundraising Report Q1 2026

2Preqin Investor Outlook: H1 2026

3Preqin, April 2026

Setting a strong pace for 2026

Our investment and exit activity continued its lively pace at the start of the year. In February, we acquired stakes in two funds, LEA II and LEA III, for our secondary programmes. LEA Partners is a German B2B-Software specialist, consolidating vertical software providers: we were an early backer of the team via our Emerging Manager programme and we have continued to build a broad investment relationship with them. The firm has a superb track record with Fund I ranked in the top decile. Fund II is expected to achieve de-risking within the next 24 months, with full liquidation taking place in the next three to four years.

In January we completed the sale of our stake in Polaris IV, as part of our active portfolio management strategy. Polaris is a leading Nordic mid-market investment firm headquartered in Denmark and its IV fund made 12 investments – six have been fully realised with the remaining six still in the portfolio. An offer on the secondary market was accepted and enabled us to crystallise attractive returns for our investors.

In March we also agreed to sell our stake in FORM alongside Diversis Capital. FORM is a SaaS mobile data collection platform used in sectors like banking, energy and food. It helps medium to large firms improve the collection, management and leverage of the data they collect. FORM was sold to Trax Retail, a portfolio company of Gemspring Capital, generating an attractive gross return.

Further information on our transactions in Q1 2026 can be found at the end of this document.

Our Emerging Manager Conference goes on tour to London

Emerging managers are becoming increasingly attractive to private equity investors. Their unique ability to outperform more established counterparts on a risk-adjusted basis makes them an excellent option for LPs looking for alpha, innovation and good returns. This advantage was clearly on show at our recent ‘Emerging Manager Conference on Tour’ event in London.

This was the first time we had brought our increasingly-popular event to London and the rapid take-up of available places highlights the sector’s strong appeal. More than 80 guests attended the conference at the Royal Society of Chemistry as we showcased cutting-edge research on the sector and engaged in thought-provoking conversations from across the emerging manager ecosystem.

During the event we were delighted to be joined by Nic Humphries, Senior Partner at Hg Capital, for a fireside chat. He shared with us Hg Capital’s incredible journey to becoming one of the world’s leading technology and services investors.

We then held two intriguing panel discussions hosted by our sponsors. The first panel with Langham Hall, asked the question every emerging manager has to face: how to launch their first fund. The panel looked at why operational setup is a key consideration for emerging managers who want to reach a first close. Participants also unpacked the primary operational challenges and considered the best route to regulation, European marketing best-practice, and the value of onshore vs offshore setups.

In the second panel, moderated by Monument Group, we shifted focus to team chemistry. When it comes to due diligence, the panel argued that team dynamics and founder disputes should be top of mind for LPs considering emerging managers. Through real-life anecdotes, the group highlighted the best practices for navigating difficult situations. They also provided some sage advice to LPs about what issues they should look out for when assessing a new management team: ego issues and conflict resolution tools were top of mind.

We also enjoyed a fascinating presentation from another of our sponsors, Addleshaw Goddard, updating us all on recent trends around legal and commercial funds terms. The team also provided observations on the regulatory landscape for emerging managers.

Back by popular demand, and for many the highlight of the day, we held two dedicated sessions to showcase great examples of emerging managers making their way in the market today. During these ‘Meet the GPs’ sessions, six up-and-coming GPs answered the same seven questions – no slides, no visuals – and tried to convince LPs in the room that theirs should be the next fund to watch. Hugely informative, these fast-paced sessions provide great examples of why we think emerging managers are worthy of more attention.

Thank you to all our sponsors and guest-speakers for another fantastic conference. We will be taking our Emerging Manager Conference on the road again – watch this space!

Mid-life deals come of age

As highlighted earlier, global exit activity remains distinctly subdued and during this prolonged dry spell, our Directs team has seen strong growth in the market for mid-life transactions. These deals have become increasingly popular in recent years as a direct result of the mismatch between the growing stock of portfolio companies and subdued exit activity, leading to longer holding periods.

Mid-life deals – those which take place during the holding period rather than at entry or final exit – are not new. When fundraising slows down significantly, interest rates rise and exits come to a near stand-still, such transactions can provide an emergency valve of liquidity. They have been recognised for some time as an efficient way for GPs to generate liquidity and inject fresh capital into an already mature asset, without necessitating a full exit into an unforgiving market or a time-consuming continuation vehicle process.

But recent market conditions and the maturation of the private equity industry in general have resulted in them moving from a niche tool to an increasingly core feature of portfolio management.

Over the past three years in particular, we have observed an increase in the quantity and sophistication of mid-life transactions and they are now regarded by GPs and LPs as a strategic tool that, when used appropriately, can help GPs preserve momentum and compound value into an asset they know well, as well as providing optionality for existing and prospective LPs. They give GPs more control over fund growth and more appropriate timing for exits and can also help to re-align investors around a fresh exit timeline. They can also provide existing LPs with a liquidity option at a fair price, as well as attract new investors. In addition, they serve to fund growth strategies that can add value and ultimately improve exit outcomes.

While mid-life deals can occur among portfolio companies of any size, their natural home is in the small and mid-market. There are several reasons why this is the case. For example, continuation vehicles (CVs), while powerful, are resource intensive and costly. Large funds can absorb this burden, but small and mid-market funds cannot. Another reason they work well in the mid-market is because smaller GPs have fewer liquidity tools at their disposal. Mid-life capital can fill this gap with efficiency and flexibility.

The increase in mid-life deals is not a temporary response to liquidity challenges. It is a more fundamental part of an increasingly-mature private equity market. It signals a shift in how private equity can preserve momentum, protect alignment and manage timing. GPs will continue to look for tools that give them more control over fund growth and exits, particularly in inconsistent exit markets and with elevated financing costs. Mid-life transactions are an attractive way of achieving that control. We are seeing a lot of benefits to all parties. LPs get exposure to mature, derisked assets with clearer upside and shorter durations while GPs can continue to support high-conviction companies. And for the companies themselves, these transactions provide capital at a crucial moment. As such, we believe mid-life capital is becoming one of the most exciting growth trends in private equity.

Unigestion Private Equity Activity

Here are the highlights of some of the investments that we completed in Q1:

In January, we commited to Cow Corner III – a Brighton-based fund manager founded in 2018 by the former Head of Business Services at HgCapital and a former Partner at HgCapital. Cow Corner is a sector specialist focusing on mission-critical, non-discretionary B2B companies within high-growth and high-IP subscription-based software and professional services verticals with high M&A potential. The firm adopts a highly operational approach, with direct involvement from the team to unlock growth through professionalisation initiatives and an enhanced focus on revenue quality, while simultaneously driving regional consolidation. Cow Corner employs a highly experienced operational team to drive performance and business excellence throughout the portfolio.

Also in January, as part of our active portfolio management strategy, we completed the sale of a stake in Polaris IV, a 2015 vintage vehicle. The fund has made 12 investments, with six fully realised and six remaining in the portfolio. Given that the fund is in its tenth year and is expected to take another two to three years to complete the exit of the remaining assets, an offer on the secondary market was accepted, crystallising attractive returns for investors. Polaris is a leading Nordic mid-market investment firm with headquarters in Denmark.

In February, we acquired two fund stakes, LEA II and LEA III, for our secondary programmes. LEA Partners is a German B2B-Software specialist, consolidating vertical software providers and has achieved an outstanding track record (Fund I is ranked top decile). The GP is one of Germany’s most successful software focused GPs, with realised 3.1x MOIC across eight historical exits. Both Fund II and Fund III offer significant remaining upside potential. Specifically, Fund II is expected to achieve de-risking within the next 24 months, with full liquidation projected within three to four years. The transaction was facilitated by the GP without involvement of an intermediary, leveraging our long-standing relationship with the GP. We have been an early backer of Lea Partners via our Emerging Manager programme and we have subsequently built a broad investment relationship with LEA across funds, co-investments and GP-led transactions.

In March, we agreed to sell our stake in FORM alongside with Diversis Capital. Form is a SaaS mobile data collection platform for complex, business-critical use cases across a broad spectrum of sectors like banking, energy and food and beverage. Its solutions have helped mid to large organisations improve how they collect, manage and leverage data, and integrate it into current systems, transforming the way they do business. During our ownership, the focus was on operational improvements and strategic growth, including the 2021 acquisition of ShelfWise, resulting in the company trippling its revenues and growing EBITA by over five times. FORM was sold to Trax Retail, a portfolio company of Gemspring Capital, generating an attractive gross return.

Also in March, we closed an investment in SAPV Care GmbH alongside Capiton. SAPV Care GmbH provides specialised outpatient palliative care for people with incurable, advanced illnesses. Its multidisciplinary team of palliative care physicians and nurses improves quality of life, alleviates symptoms such as pain and shortness of breath, and enables patients to live with dignity until the end of their lives in the comfort of their own homes. The company operates seven locations across Rhineland-Palatinate and Saarland, covering 49 service areas with 110 employees. The specialized outpatient palliative care market is expected to continue growing at ~7% p.a. Key drivers include, demographic change, rising complex disease prevalence, and cost pressure shifting care to outpatient settings which provides regulatory tailwinds.

Contact Us

| sagard | |

| [email protected] |

INFORMATION ONLY FOR YOU

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

RELIANCE ON UNIGESTION

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time. Such information is intended to provide you with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf of one or more Unigestion entities will be involved in managing any specific client account on behalf of another Unigestion entity.

NOT A RECOMMENDATION OR OFFER

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision. Reference to specific securities should not be construed as a recommendation to buy or sell such securities and is included for illustration purposes only.

RISKS

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Unigestion maintains the right to delete or modify information without prior notice. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, and may experience substantial & sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

PAST PERFORMANCE

Past performance is not a reliable indicator of future results, the value of investments, can fall as well as rise, and there is no guarantee that your initial investment will be returned.

If performance is shown gross of management fees, you should be aware that the inclusion of fees, costs and charges will reduce investment returns.

Returns may increase or decrease as a result of currency fluctuations.

NO INDEPENDENT VERIFICATION OR REPRESENTATION

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

FORWARD-LOOKING STATEMENTS

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. You are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

TARGET RETURNS

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events and are subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. You are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Target returns and/or forecasts are based on Unigestion’s analytics including upside, base and downside scenarios and might include, but are not limited to, criteria and assumptions such as macro environment, enterprise value, turnover, EBITDA, debt, financial multiples and cash flows. Targeted returns and/or forecasts are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

If target returns, forecasts or projections are shown gross of management fees, the inclusion of fees, costs and charges will reduce such numbers.

USE OF INDICES

Information about any indices shown herein is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison. You cannot invest directly in an index and the indices represented do not take into account trading commissions and/or other brokerage or custodial costs. The volatility of the indices may be materially different from that of the strategy. In addition, the strategy’s holdings may differ substantially from the securities that comprise the indices shown.

HYPOTHETICAL, BACKTESTED OR SIMULATED PERFORMANCE

Hypothetical, backtested or simulated performance is not an indicator of future actual results and has many inherent limitations. The results reflect performance of a strategy not currently offered to any investor and do not represent returns that any investor actually attained. One of the limitations of hypothetical performance results is that they are generally prepared with the benefit of hindsight.

Hypothetical performance may use, among other factors, historical financials (turnover, EBITDA, debit, financial multiples), historical valuations, macro variables and fund manager variables. Hypothetical results are calculated by the retroactive application of a model constructed on the basis of historical data and based on assumptions integral to the model which may or may not be testable and are subject to losses. Changes in these assumptions may have a material impact on the hypothetical (backtested/simulated) returns presented. Certain assumptions have been made for modeling purposes and are unlikely to be realized. No representations and warranties are made as to the reasonableness of the assumptions.

This information is provided for illustrative purposes only. Specifically, hypothetical (backtested/simulated) results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Hypothetical trading does not involve financial risk, and no hypothetical trading record can completely account for the impact of financial risk in actual trading. For example, the ability to withstand losses or to adhere to a particular trading program in spite of trading losses are material points which can also adversely affect actual trading results. Since trades have not actually been executed, results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity, and may not reflect the impact that certain economic or market factors may have had on the decision-making process. Further, backtesting allows the security selection methodology to be adjusted until past returns are maximized.

If hypothetical, backtested or simulated performance is shown gross of management fees, the inclusion of fees, costs and charges will reduce such numbers.

ASSESSMENTS

Unigestion may, based on its internal analysis, make assessments of a company’s future potential as a market leader or other success. There is no guarantee that this will be realised.

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

In the United States, Unigestion is present and offers its services in the United States as Unigestion (US) Ltd, which is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”), which is registered as an investment advisor with the SEC. All inquiries from investors present in the United States should be directed to [email protected]. This information is intended only for institutional clients that are qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).