Stephen Harvey

Chief Investment Officer

Sagard Wealth

A happy Victoria Day weekend to those of you in provinces that celebrate Queen Victoria’s birthday and a happy Journée nationale des patriotes to those in Québec. Maybe some of you will be visiting the United States this weekend and complaining about the Canadian Dollar equivalent prices. Help may be at hand with a weaker U.S. Dollar.

DXY

How should we think about the performance of the U.S. dollar? The answer depends heavily on where you sit. A Canadian investor, a European exporter, a Japanese policymaker, and an emerging-market borrower will all experience “dollar strength” differently.

The most common market shorthand is the DXY, or U.S. Dollar Index. It measures the dollar against a basket of six developed-market currencies. The basket is heavily weighted toward Europe, which is important. DXY is useful, widely followed, and tradable, but it is not a perfect reflection of today’s U.S. trade relationships.

The current DXY weights are:

• Euro: 57.6%

• Japanese yen: 13.6%

• Pound sterling: 11.9%

• Canadian dollar: 9.1%

• Swedish krona: 4.2%

• Swiss franc: 3.6%

The most notable omissions are the Chinese yuan and Mexican peso, despite China and Mexico being major U.S. trading partners. That is one reason I view DXY as a good market indicator, but not a complete measure of the dollar’s global trade impact. ICE describes DXY as a six-currency, geometrically averaged index, and the euro alone represents more than half of the basket.

Dollar and Presidents

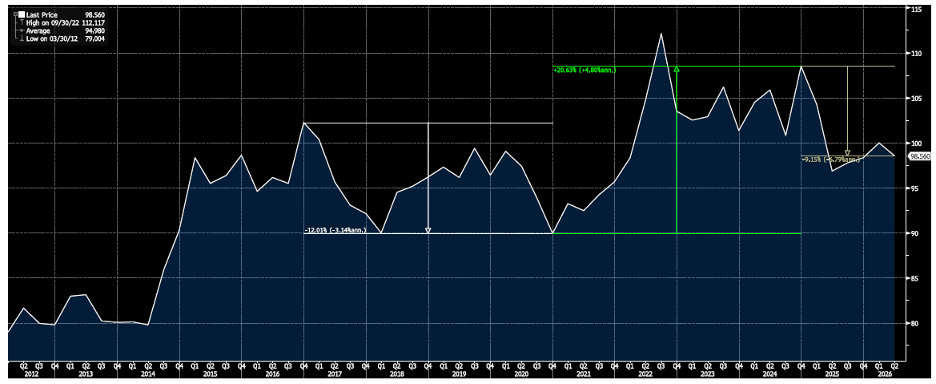

The chart below shows DXY performance over the past 12 years. When the index rises, the dollar is strengthening versus the basket. When the index falls, the dollar is weakening.

Source: Bloomberg

What stands out is the degree to which the dollar has moved through very different political, fiscal, and monetary backdrops.

During Trump’s first term, from January 2017 to January 2021, DXY weakened by roughly 12%. That period included tax reform, tariffs, trade renegotiation, and a generally more explicit preference for a competitive dollar. Those policies were not the only drivers, but the policy mix leaned in a direction that was broadly consistent with a weaker dollar.

During Biden’s term, from January 2021 to January 2025, the dollar strengthened by more than 20%. The biggest driver was monetary policy. Inflation proved stronger and more persistent than expected, forcing the Federal Reserve into one of the sharpest hiking cycles in decades. The effective fed funds rate was near zero from April 2020 through March 2022, then moved above 5% during 2023. Higher U.S. rates increased the return available on dollar cash and short-dated Treasuries, pulling capital toward the U.S. and supporting the dollar.

So far in Trump’s second term, the dollar has weakened again. DXY is down about 9% from inauguration, which means that across the full period since Trump first took office in 2017, the dollar has moved in a wide range but is not far from where it began.

A Weaker Dollar Helps Some Objectives

A weaker dollar is not universally good. It can raise import prices, pressure consumers, and complicate the inflation picture. But it does align with several objectives of the current administration.

First, a weaker dollar makes imported goods more expensive, which can shift some demand toward domestically produced goods.

Second, it makes U.S. exports cheaper for foreign buyers, helping American companies compete abroad.

Third, it can support the foreign earnings of U.S. multinationals. When overseas revenues are translated back into dollars, a weaker dollar can provide a tailwind to reported earnings.

The trade deficit remains central to this discussion. The U.S. continues to import more than it exports. The latest monthly goods and services deficit was $60.3 billion in March 2026, while the three-month average deficit was $57.6 billion. That pace is below the 2024 and 2025 annual goods-and-services deficits, though the goods deficit alone remains much larger.

Why Has the Dollar Weakened?

There are several reasons.

The first is trade policy. Tariffs and the threat of tariffs have created noise around import activity. Some companies pulled imports forward ahead of policy changes, while others have since adjusted supply chains or reduced activity. Trade data have become more volatile, but the direction of travel has been toward lower import momentum relative to last year. Year-to-date through March, the goods and services deficit was down 55% versus the same period in 2025, with exports higher and imports lower.

The second is relative interest rates. Currency markets are heavily influenced by the return investors can earn in one currency versus another. When U.S. rates are rising faster than the rest of the world, the dollar tends to attract capital. When the Fed is expected to cut, or when other central banks become relatively more attractive, that support fades.

The third is debt issuance. The U.S. has been running large fiscal deficits, financed by heavy Treasury issuance. That does not automatically weaken the dollar, but it does mean the U.S. needs continuous demand from domestic and foreign buyers. If marginal foreign demand softens, the dollar can lose one of its supports.

Finally, positioning matters. The dollar entered this period with a lot of good news already priced in – U.S. growth exceptionalism, higher U.S. rates, and global demand for dollar assets. When a crowded trade begins to unwind, the currency can move quickly.

Portfolio Implications

Despite still elevated inflation, I expect the dollar to remain under pressure.

A weaker dollar is generally supportive of emerging markets, especially countries and companies with dollar-denominated debt. When the dollar falls, the local-currency burden of that debt declines.

It is also supportive of commodities. Most major commodities are priced in dollars, so a weaker dollar tends to improve affordability for non-U.S. buyers and can provide a tailwind to commodity prices.

The investment takeaway is straightforward: the dollar is no longer the one-way tailwind it was during the Fed hiking cycle. If dollar weakness continues, it should improve the backdrop for non-U.S. assets, emerging markets, commodities, and globally diversified portfolios.

The greenback has not broken. But it has been greenbucked.