Stephen Harvey

Chief Investment Officer

Sagard Wealth

It was great to see so many of you at the Calgary Stampede last week. To quote Rage Against the Machine, “the bulls were certainly on parade!”

Since 2020 the equity bulls have generally run hard, but why is this? How much impact have policymakers had over that period? In the below piece we ask the question whether the traditional 60:40 portfolio (60% equities and 40% bonds) is broken?

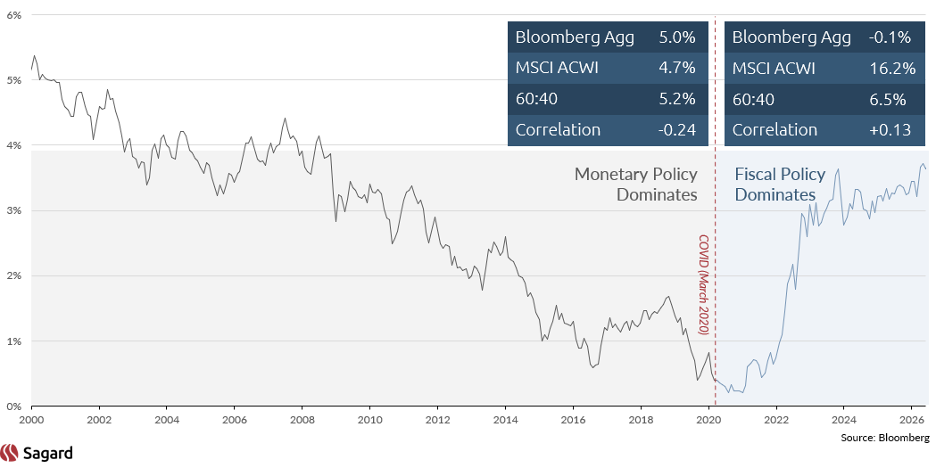

From 2000 to 2020, monetary policy dominated markets. Over that period, G7 government bond yields declined with remarkable consistency. When market stress emerged, central banks repeatedly came to the rescue, using interest-rate cuts and quantitative easing as the primary policy tools.

This created an exceptionally favourable backdrop for the traditional 60:40 portfolio. Falling bond yields drove bond prices higher, while equities compounded through the cycle despite several major dislocations. Bonds also maintained a modestly negative correlation to equities, allowing them to provide both positive expected returns and meaningful downside protection. It was, in many respects, a golden era for the 60:40 framework.

That regime began to shift in March 2020. COVID required a different policy response. The shock was not simply financial; it was income, labour market, and real-economy shock. Governments therefore had to step in directly, using fiscal policy to replace lost household income and support businesses through the shutdown period.

In the years that followed, fiscal policy became the dominant market force. At the same time, government bond markets faced two powerful headwinds: first, a significant increase in sovereign issuance, which raised the supply of debt; and second, a surge in inflation, which reduced the demand for duration at prevailing yields.

The result has been a very different environment from the prior two decades. Government bonds have generated weak, and in some cases negative, returns, while equities have continued to outperform. More importantly, bonds have shifted from being negatively correlated with equities to being positively correlated at key points in the cycle. That change has undermined their traditional role within the 60:40 portfolio, reducing their effectiveness as both a return generator and an equity-risk diversifier.

The chart below shows this with the line showing the average 10-year bond yield across the G7 over the last 26 years:

We believe the focus should be on rebuilding the defensive allocation, rather than simply relying on the traditional 40% bond sleeve to play the same role it did in the past. In a world where government bonds are more vulnerable to inflation, fiscal deficits, and shifts in term premia, investors need to broaden their sources of income and diversification.

That means replacing part of the traditional bond allocation with alternative sources of income. Strategies such as private credit and hedge funds can offer a bond-like return profile, but with lower sensitivity to interest rates and less dependence on falling yields to generate returns. These strategies may also provide exposure to different risk premia, including credit complexity, illiquidity, manager skill, relative value, and market dislocation.

The key is not to abandon defensive assets altogether. Rather, it is to recognize that the composition of the defensive portfolio needs to evolve.

In the prior regime, duration did much of the work. In the current regime, income, flexibility, and alternative risk premia should play a larger role. Fiscal policy is likely to continue to dominate as debt piles rise. Investors will need different tools.